September 19, 2025

Tata Motors Launches Ace Gold+ Diesel Mini-Truck at Rs. 5.52 Lakh*

Read moreTata Motors Ltd announced its results for quarter ending December 31, 2022. The results represent the details on consolidated segment level.

| Consolidated (₹ Cr Ind AS) |

Jaguar Land Rover (£m, IFRS) | Tata Commercial Vehicles (₹Cr, Ind AS) |

Tata Passenger Vehicles (₹Cr, Ind AS) |

||||||

|---|---|---|---|---|---|---|---|---|---|

| FY23 | Vs. PY | FY23 | Vs. PY | FY23 | Vs. PY | FY23 | Vs. PY | ||

| Q3 FY23 |

Revenue | 88,489 | 22.5 % | 6,041 | 28.1 % | 16,886 | 22.5 % | 11,671 | 37.4 % |

| EBITDA (%) | 11.1 | 90 bps | 11.9 | (10) bps | 8.4 | 580 bps | 6.9 | 370 bps | |

| EBIT (%) | 4.4 | 270 bps | 3.7 | 230 bps | 5.9 | 650 bps | 1.5 | 510 bps | |

| PBT (bei) | 3,203 | ₹3,901 crs | 265 | £274m | 938 | ₹1,093 crs | 321 | ₹650 crs | |

| YTD FY23 |

Revenue | 240,035 | 20.0% | 15,707 | 15.9 % | 49,576 | 46.9 % | 35,775 | 70.2 % |

| EBITDA (%) | 9.5 | 50 bps | 9.8 | 20 bps | 6.3 | 380 bps | 6.1 | 170 bps | |

| EBIT (%) | 2.2 | 250 bps | 0.5 | 170 bps | 3.7 | 500 bps | 0.9 | 460 bps | |

| PBT (bei) | (3,533) | ₹3,214 crs | (432) | £(11)m | 1,531 | ₹2,271 crs | 503 | ₹1,401 crs | |

Jaguar Land Rover (JLR): JLR delivered on its plans and achieved positive free cash flow and profitability in the quarter as supplies improved. Revenues were £6.0 billion, up 28% vs. Q3 FY22 and up 15% sequentially reflecting better supplies, strong model mix and pricing. Profit before tax in the quarter was £265 million, up from a loss of £(9) million a year ago with a positive EBIT margin of 3.7%, up from 1.4% in Q3 FY22. The higher profitability reflects increased wholesale volumes with favourable mix, pricing and foreign exchange offset partially by higher inflation and supplier claims largely related to constrained volumes. Free cash flow was £490 million in Q3 FY22.

Tata Commercial Vehicles (Tata CV): Tata CV revenues in Q3 FY23 were up 22.5% vs. Q3 FY22 at ₹ 16.9KCr. Q3 FY23 EBITDA margins were 8.4% (+580 bps yoy) and EBIT margins were at 5.9% (+ 650 bps y-o-y) led by better mix, higher realisations, cost savings and softened commodity prices. The business was PBT (bei) positive at ₹ 0.9K Cr as compared to loss of ₹ 0.2K Cr in Q3 FY22.

Tata Passenger Vehicles (Tata PV): Tata PV revenues were up 37% vs Q3 FY22 at ₹ 11.7K Cr reflecting higher volumes and realizations. EBITDA margins were 6.9% (+370 bps yoy) and EBIT margins were at 1.5% (+510 bps) yoy driven by improved volumes and mix, higher realizations, softening commodities and certain one offs. The business was PBT (bei) positive at ₹ 0.3K Cr as compared to loss of ₹ 0.3K Cr in Q3 FY22.

Outlook: We remain cautiously optimistic on the demand situation despite global uncertainties. We will remain vigilant on demand and our continued focus on profitable growth, improving semiconductor supplies and stable commodity prices will aid revenue growth, margin improvement and positive cash delivery in Q4 FY23.

JAGUAR LAND ROVER (JLR)

Highlights

REIMAGINE TRANSFORMATION CONTINUES

Looking Ahead

The Company continues to see strong demand for its vehicles. Wholesales in China during the quarter were impacted by lockdowns leading to dealer closures followed by high rates of staff absence as Covid-19 restrictions were relaxed. The situation is expected to recover in the fourth quarter with our dealers open and staff absence closer to normal levels in January. The Refocus transformation programme is on track to deliver a target of £1 billion plus improvements in the year to help mitigate the impact of inflation.

Although there continues to be supply chain and other macro risks, our guidance for the full year remains unchanged. Positive EBIT margin and free cashflow in Q4 FY23 on wholesales of 80,000 or more are expected to achieve breakeven free cashflow and a positive EBIT margin for the full year.

Adrian Mardell, Jaguar Land Rover’s Interim Chief Executive Officer, said: “JLR has returned to profit as chip shortages eased in the quarter and production and wholesales increased. These improved results are testament to the hard work and dedication of our people across the business who have delivered a further increase in production of our New Range Rover and Range Rover Sport models.

We remain committed to our Reimagine strategy which will transform JLR into an all-electric modern luxury business, whilst delivering our SBTi climate goals and striving to exceed our clients’ expectations.”

TATA COMMERCIAL VEHICLES (TATA CV)

Highlights

Financials

The commercial vehicles industry witnessed a robust recovery in Q3 FY23 led by strong demand in MHCV and passenger carrier segment. Improving fleet utilizations, pick up in road construction projects and increase in cement consumption catalyzed the demand recovery for MHCVs. CV exports, however, remained subdued due to the prevailing economic situation in most of our overseas markets. Domestic wholesales were at 90.8k units (flat yoy), domestic retails at 97.7k units (+5%). Our continued focus on retail during the quarter resulted in retail sales surpassing wholesale by 6.3% in Q3 FY23, and reducing system inventory as we transition towards BSVI phase-2 norms.

Revenues at ₹ 16.9KCr was up 22.5% yoy despite wholesales being down 6%, reflecting improved mix and better market operating price. Q3 FY23 EBITDA margins were 8.4% (+580 bps yoy) and EBIT margins were at 5.9% (+ 650 bps yoy) led by sustained pricing improvement, cost actions and softening commodity prices. The business was PBT (bei) positive at ₹ 0.9K Cr as compared to loss of ₹ 0.2K Cr in Q3 FY22.

Looking Ahead

The CV industry is poised for growth on the back of increased infrastructure activity, demand for last mile mobility and strong recovery in bus segment. Going forward, we expect a good replacement demand, especially in MHCVs in Q4 FY23, as we also maintain a close watch on the evolving geopolitical situation, inflation and interest rate risks on both the supply and demand. The recent exciting launches of the new range of smart trucks in MHCV and ILCV, and best-in-class pickups will help us serve our customers better. We exhibited most comprehensive range of greener and zero emission mobility solutions at Auto Expo, across cargo and passenger segments, powered by natural gas, electric and hydrogen.Focus will continue to remain on registration market share improvement with demand-pull strategy, innovation intensity, restoring double-digit EBITDA margins and successfully delivering on new business models.

Girish Wagh, Executive Director Tata Motors Ltd said: “In Q3 FY23, the CV industry witnessed a steady, overall demand. Our focus on creating ‘’Demand Pull’ from customers and sustained emphasis on retail in Q3 FY23 resulted in retail sales surpassing wholesale by 6.3%, thereby enabling reduction in inventory as we transition towards BS VI phase-2 norms. Led by realization improvement, revenue growth was higher than volume growth. Realization improvement coupled with commodity softening and cost control resulted in improved margins. Going forward, we will maintain our agility and keep a close watch on the evolving geopolitical, inflation and interest rate risks on both supply and demand. We will also continue to drive the business with strong customer connect, product and service innovations to improve customer affinity for our brands, step-up registration market shares sustainably, and improve realisations and profitability.”

TATA PASSENGER VEHICLES (TATA PV)

Highlights

Financials

Tata PV business continued its strong momentum in Q3 FY23. Wholesales grew 33% yoy to 132.3k vehicles driven by strong demand for Nexon, Nexon EV, Punch, Tiago and Tigor CNG. Retails grew 27% yoy. The business witnessed highest ever retails at 139K. The revenues grew 37% yoy to ₹ 11.7K Cr reflecting higher volumes and realizations. EBITDA margins were 6.9% (+370 bps yoy) and EBIT margins were at 1.5% (+510 bps yoy) driven by improved volumes & mix, realizations, softening commodities and certain one off’s. The business was PBT (bei) positive at ₹ 0.3K Cr as compared to loss of ₹ 0.3K Cr in Q3 FY22. Market share improved to 14.1% in YTD FY23.

Looking Ahead

While in Q3 FY23 the industry witnessed some moderation in demand post festive season, we expect the PV industry to continue witnessing robust demand in the next quarter. We expect the growth momentum for EVs to remain strong with their rising popularity and the announcement of progressive policies by several states. The Company has commenced deliveries of Tiago.ev in January 2023 and strong 20K+ order book will support growth. The Company unveiled range of exciting new offerings at auto expo, including Avinya, Harrier EV, Sierra EV, ICE Curvv, Punch and Altroz with twin iCNG technology which received an overwhelming response. The Company will continue to deliver market-beating growth, improve profitability and cash flows.

Shailesh Chandra, Managing Director Tata Motors Passenger Vehicles Ltd & Tata Passenger Electric Mobility Limited said: “Q3 FY23 was one of the best quarters for the PV industry with strong retails from new launches, robust festive demand, and adequate supply of vehicles. Tata Motors posted its highest ever quarterly retails in Q3 FY23 and crossed the 50,000 units of monthly retail for the first time. Wholesales of 131,297 units recorded in Q3 FY23 (+32.6% vs Q3 FY22) resulted in the business comfortably crossing the distinctive landmark of 500,000 annual units to post wholesale of 526,798 units in CY22. EVs too posted their highest ever sales in Q3 FY23 at 12,596 units (+ 116.2% vs Q3 FY22) and crossed the cumulative sales milestone of 50,000 units. Going forward, we remain vigilant about the evolving demand and supply situation and will stay nimble to take necessary actions swiftly whilst focusing on improving profitability further.”

ADDITIONAL COMMENTARY ON FINANCIAL STATEMENTS

(Consolidated Numbers, Ind AS)

Finance Costs

Finance costs increased by ₹ 275 Cr to ₹ 2,676 Cr during Q3 FY23 as compared to ₹2,401 Cr in Q3 FY22 due to higher gross borrowings.

Joint ventures, Associates and Other income

For the quarter, net profit from joint ventures and associates amounted to ₹103Cr compared with a loss of ₹ 113Cr in Q3 FY 22. Other income (excluding grants) was ₹ 455Cr in Q3 FY23 versus ₹ 197Cr in Q3 FY22.

Free Cash Flows

Free cash flow (automotive) in the quarter, was positive at ₹ 5.3K Cr (as compared to ₹ 4.0K Cr in Q3 FY 22) owing to improvement in cash profits and working capital.

REPORTING FORMAT

The press release represents the details on consolidated segment level. The operating segment comprise of automotive segment and others.

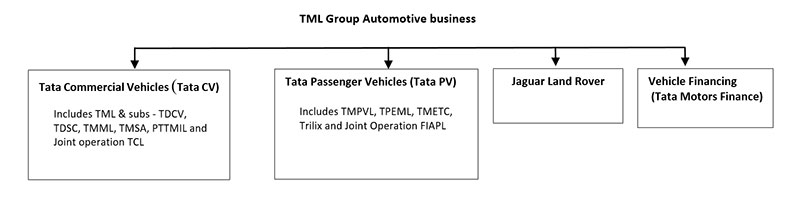

In automotive segment, results have been presented for entities basis four reportable sub-segments as below